CrowdStrike Holdings - Q421 & Full Year 2021 Earnings Update

CrowdStrike Holdings - Q421 & Full Year 2021 Earnings Update

Large Cap Cloud Security - Record Quarter & Increasing Deal Activity; Long-Term Trends Very Attractive; Cautious on Valuation

Disclosure: We do own a long position in CRWD. Please read the remaining disclosures at the bottom of this post.

CrowdStrike Holdings (CRWD) announced fourth quarter and full year 2021 earnings yesterday evening. We have updated our estimates below to reflect the results and have included our thoughts on the quarter as well as notes from the company conference call.

Company Description

CrowdStrike provides cloud-delivered next-gen endpoint security. Leveraging the network effects associated with crowdsourced data applied to modern technology such as artificial intelligence (AI), cloud computing and graph databases, the CrowdStrike Falcon platform offers the first multi-tenant, cloud native, intelligent security solution capable of protecting workloads across on-premise, virtualized, and cloud-based environments running on a variety of endpoints such as laptops, desktops, servers, virtual machines, and IoT devices. The company operates through a software as a service (SaaS), subscription-based model. The company is run by its co-founder, George Kurtz and is headquartered in Sunnyvale, CA.

Business Overview

CrowdStrike reported another strong quarter with beats across the board. Customers of all sizes continue to choose CrowdStrike for their cloud security platform needs. Recent events, including the Sunburst security software supply chain attack highlight the needs for security beyond traditional endpoint detection and response (EDR). CrowdStrike continues to enhance their platform capabilities, including their timely acquisition of Preempt to get ahead of these industry trends. CrowdStrike also completed their most recent acquisition, the purchase of Humio. CEO George Kurtz highlighted the purchase as “a key element of [their] strategy to drive long-term growth”. The purchase will fuel continued innovation to what CRWD believes to be the “fastest, most cost-efficient, and extensible cloud data platform that will deliver best-in-class visibility for security, as well as observability for IT operations”.

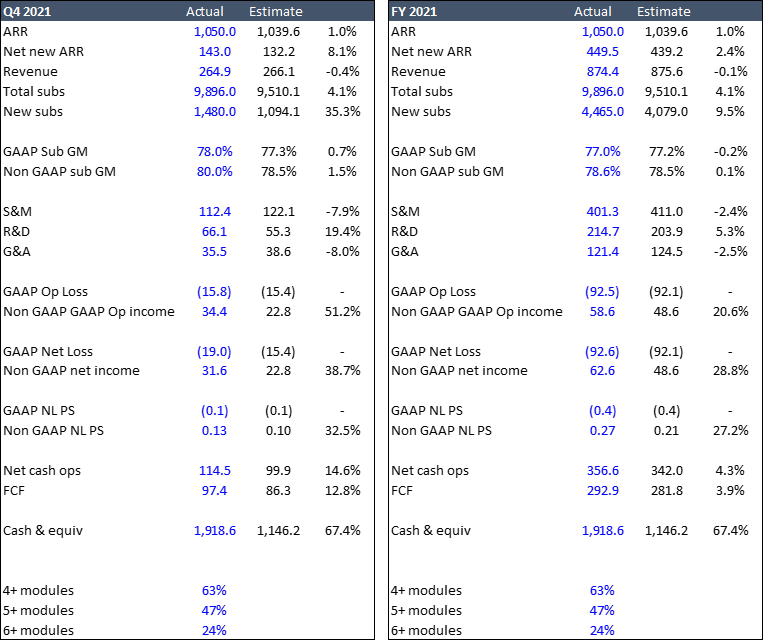

The fourth quarter topped of an extremely strong year for CRWD, delivering exceptional growth at scale, margin improvements and meaningful free cash flow margins. In the year, the company reached the milestone of annual recurring revenue (ARR) crossing over $1B, +75% YoY. They believe this makes them the third fastest cloud-native SaaS company to report $1B ARR, following only Salesforce and Zoom, both of which are now CRWD customers following the addition of Salesforce in Q4.

The company delivered record net new ARR in the quarter of $143M and reported subscription revenue growth of 77%, highlighting the continued momentum in demand for the platform. In terms of internal growth, the company continues to see rapid module adoption, with the number of customers adopting 4, 5 or 6 modules reaching 63%, 47% and 24%, respectively. Externally, the go-to-market strategy continues to gain traction amidst strong secular trends for the industry at large. The company added a record 1,480 net new subscription customers in the quarter, bringing their total to 9,896 subscription customers worldwide.

Within the quarter, CRWD added a number of large enterprises to their customer base, including the likes of Pfizer (PFE) and Proctor & Gamble (PG). The company also highlighted some market share wins, mentioning a large technology company where CRWD will be replacing a competitor, SentinelOne. The replacement was based on SentinelOne not being scalable for the technology company needs, which led to dramatically reduced performance and causing lower developer productivity. CRWD also announced foundational customer adds in the federal space with a major defense contractor.

The company also had success with their partnerships, growing their partnership count by 85% worldwide and doubling the number of partner-sourced transactions. The partnership with AWS contributed materially, with ARR transacted through AWS growing 650% over the last year with transaction volumes growing over 300%.

Following the Sunburst attacks, there has been a wave of customer interest in protecting their cloud directories. This interest is driving demand for identity protection technologies such as CRWD’s Zero Trust offerings derived from the purchase of Preempt. With Preempt Security, CRWD delivers a Zero Trust solution focused on endpoints and workloads. Preempt expands CRWD’s Zero Trust offerings and incorporates critical identity behavior data and analysis to help customers fortify their defense and prevent identity-based attacks or insider threats. The initial phase of integration with Preempt is on track for Q1 and the management team is pleased with the early indications of interest.

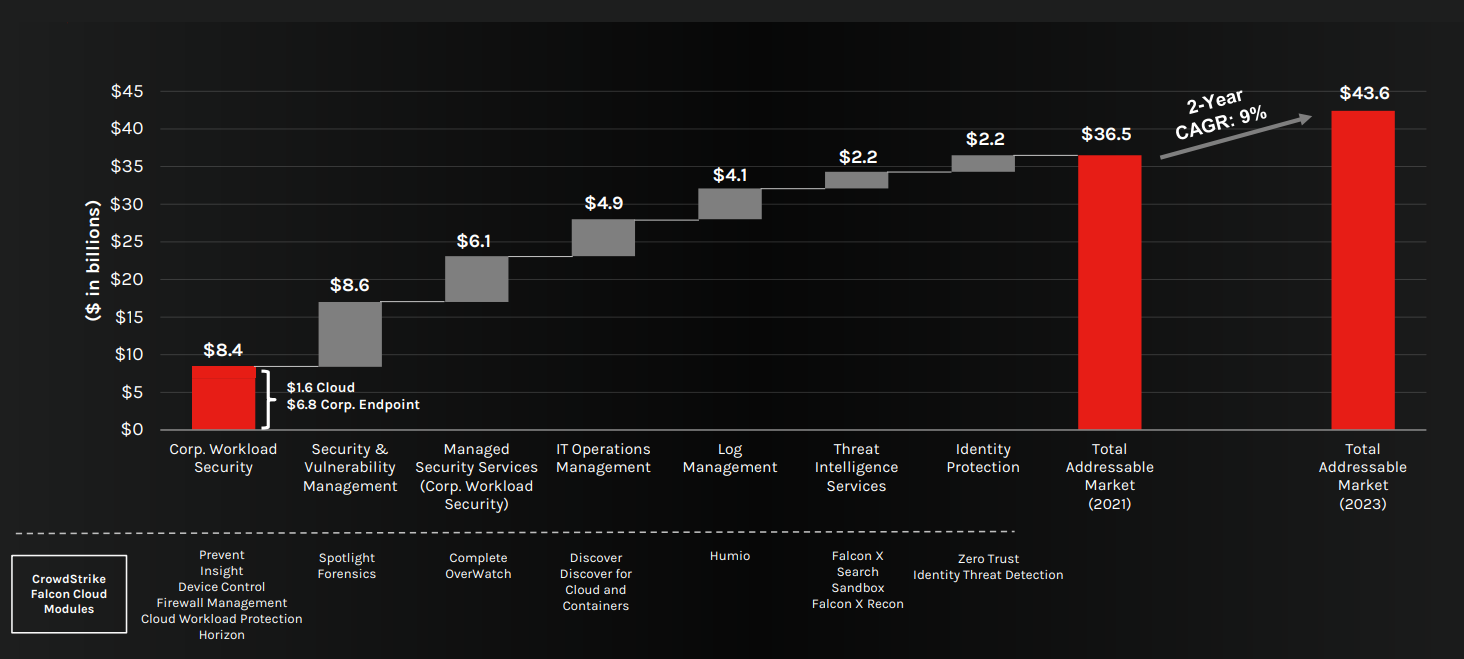

The company also completed their purchase of Humio, a next-gen XDR provider. Humio provides CRWD the ability to expand their data lake, allowing them to see more data and therefore solve more security use cases in real time. Humio capabilities will be built into the fabric of the CRWD Falcon OverWatch, Complete and threat intelligence modules, adding a data and time advantage over competition. On day one of the integration, Humio will broaden the reach of CRWD into the log management market. This market alone is forecasted to be ~$5B in 2023 (based on IDC estimates), bringing CRWD TAM to ~$43.6B.

Based on Mr. Kurtz comments (summarized above), it seems clear that the CRWD platform continues to gain traction in this extremely large and competitive space. The company has continued to invest in the platform offerings and the efforts of their professional service and operational teams are highlighted by the record net new ARR and subscription customers gains in the quarter. Further, the additions of Preempt and Humio will provide meaningful additions to TAM and will broaden out the growth potential over the medium to long-term for the business. On a more macro scale, the tailwinds from the pandemic (with work from home driving businesses to the cloud) continue to be strong and customer engagement continues to increase, giving us conviction in CRWD for the long-term.

Financial Highlights

CRWD reported extremely strong financial results for the full year 2021, reporting revenue growth of 82%, 7% operating margin and 33% free cash flow margin. They are exiting the year with record subscription gross margin and free cash flow in the fourth quarter of $97M. Success throughout the year was broad based, with demand across multiple areas of the business. Similar to previous quarters, success was mixed between internal (cross sale) and external growth, all across enterprise and SMB accounts. Their land-and-expand strategy has been a continued success, recording dollar-based net retention of 125% in FY2021, up from 124% at the end of FY2020.

From a top-line perspective, the business continues to thrive across its revenue-generating units. Total revenue grew 74% YoY, with the subscription business posting 77% YoY growth and the professional services businesses posting 49% YoY growth. International expansion continues to show promise, with EMEA +84% YoY and APAC +113% YoY.

The business model continues to generate operating leverage and reap the benefits of scale. For the fourth quarter, non-GAAP gross margin improved to a record 77%, +380bps YoY. Non-GAAP subscription gross margin increased to 80%, up from 77% in the fourth quarter of last year. Operating expenses as a percent of revenue improved throughout the year, improving by ~17%points, with both R&D and G&A within the company’s long-term target model. The leverage throughout the year highlights the efficiency of their business model and enables them the leeway to step up investments in new initiatives, new geographies and continued marketing efforts. Fourth quarter non-GAAP operating profit reached $34.4M, representing the ninth straight quarter of operating profit improvement. Non-GAAP net income for the quarter was $31.6M or $0.13 on a diluted per share basis. Non-GAAP net income for the year totaled $62.6M or $0.27 per diluted share.

The company ended the fourth quarter with a solid balance sheet, with cash and equivalents totaling ~$1.9B, reflecting the net proceeds from their unsecured note offering in January totaling ~$740M. The company continues to improve on the cash flow front, recording record OCF and FCF in the fourth quarter.

1Q22 & 2022 Guidance

Note: the below guidance includes the addition of Humio, which closed on March 5th, 2021. Management expects Humio contribution to net new ARR to be ~$2M in the first quarter. Humio was purchased with cash on hand and will represent ~$352M (net of cash acquired) and will be reflected in Q1 2022 results. Interest expense related to the issuance of $750M of unsecured notes and the $750M expansion of their undrawn credit line to total to ~$22.6M per year, excluding amortization of debt issuance and debt issue discounts.

Revenue Q1 2022: $287.8 - $292.1M; FY 2022: $1,310.4 – $1,320.7M

Non-GAAP Operating Income Q1 2022: $18.5 - $21.7M; FY 2022: $94.8 – $102.5M

Non-GAAP Net Income Q1 2022: $10.8 – $13.9M; FY 2022: $63.8 – $71.4M

Non-GAAP EPS (diluted) Q1 2022: $0.05 - $0.06; FY 2022: $0.27 - $0.30

Additional Comments

On some of the customer wins in the quarter, Mr. Kurtz mentioned that nearly across the board, whether CRWD is displacing a next-gen or a legacy provider, the rationale from customers have been centered on the ease of use and the scalable nature of the platform. He mentioned recent rollouts for financial services companies and feedback has been extremely positive: “it’s been the smoothest rollout that they’ve seen… and the amount of visibility that [CrowdStrike has] is unbelievable compared to [their] competitors”. This feedback reiterates our conviction in our original thesis. We initiated our position in CRWD based on its differentiated nature; being born in the cloud reduces friction in adding new modules, which has created an extremely attractive incremental gross margin profile in the high 80%’s. The cloud-native structure has created a unique moat in a highly competitive industry and the moat is bearing fruits today and we expect this strength to continue.

On the partnership with EY – the partnership with EY has been bearing fruit very early on. EY has very deep ties to corporations and is guiding them as they digitally transform. Management is extremely excited about the EY partnership and feels it offers them an edge as EY operates at the board level, offering a unique look-through to the pulse of board rooms. Further, the relationship with EY is worldwide in nature, which will assist CRWD in their continued penetration of offshore markets. As the company progresses, there is a possible path to a 50/50 revenue split between on and offshore. With the continued nurturing of the AWS and EY relationships, CRWD is seeing increased progress in the offshore space. Other companies in this industry, with maturity, have reached a revenue split of ~50/50 and Mr. Kurtz sees that as a legitimate possibility over the medium term.

Mr. Kurtz called the current threat environment the worst he has seen in a long time. With regards to the SolarWinds attack, he said it was the most significant event he’d seen in almost 30 years in the security business. Taking this into account in conjunction with the trust concerns with Microsoft and Sunburst, there is a long-term trend with customers migrating to better technology with more visibility which will pose a tailwind for the EDR and XDR capabilities of CRWD. The addition of Preempt is very timely in that way, as the addition of the Zero Trust modules are better tech that offer that increased visibility.

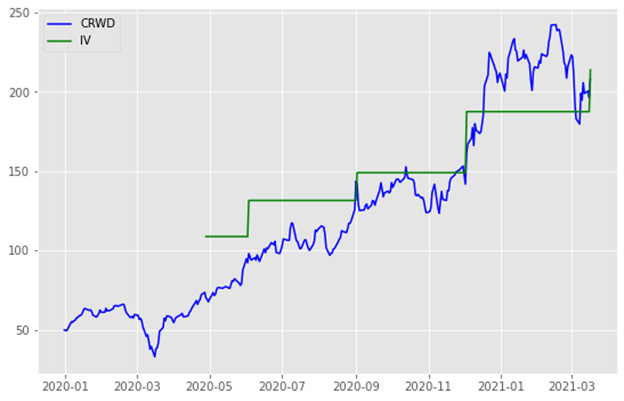

Valuation & Intrinsic Value Update

We value CRWD with a 10Y DCF Model. We apply a WACC of 8.5% to forecasted FCF through FY 2031 and apply a terminal EV/FCF multiple of 18.7x. These assumptions yield a $213 intrinsic value per equity share, ~3% from spot (3/17/2021). This equity value implies a ~23x EV/Revenue in FY 2023, which is still a bit rich for our liking in terms of adding additional capital. The stock is a favorite in the SaaS community and trades at a premium given the growth of the business and operational execution they have shown to date. We had entered the name when it was trading for ~15-17x EV/Revenue and would expect continued multiple contraction in the case of rising interest rates. Companies with high free cash flow generation in out years of DCF models are highly sensitive to changes in interest rates and we have seen this dynamic play out YTD. With that said, we continue to hold the position and are very optimistic on CRWD. Given the current valuation and interest rate risks associated with high-growth names, we would be cautious at current valuations.

Model Summary

DCF Model

Risks to the estimate include:

Competition – The cloud security market, notably EDR markets are highly fragmented and competitive. With a handful of legacy vendors being displaced by next-gen solutions, innovation and technology leadership is key to operational success. While we view CRWD as a leader in the space, any material enhancement to technology that CRWD does not take part in or lead may cause a deterioration in the thesis.

Operational execution – CRWD has yet to be profitable on a GAAP basis in terms of operating or net income. While non-GAAP metrics are positive, there is no certainty that CRWD will be able to achieve GAAP profitability. We do not expect gap profitability until FY2023. With rapid growth, operational execution and margin expansion will be key to CRWD success going forward. Any deterioration in profitability will cause us to reevaluate the thesis.

New module launches and international expansion – The success of the business is dependent on their ability to launch successful modules on the platform and continue their expansion offshore. Any deterioration in their growth strategy would lead to a reevaluation of the thesis.

Valuation – As we touched on in the valuation section, high growth names like CRWD which are often valued using DCF models inherently carry a high sensitivity to changes in interest rates. As rates rise, the discount rates used in the model will increase thus hurting the multiples applied to terminal free cash flows, and with it, the valuation. We have already seen a correction in high-growth equities in the early months of 2021 which brought on multiple contraction as the US 10 year moved from ~90bps to ~165bps. Any material move upward in rates may lead to continued multiple contraction and cause adverse price action in CRWD equity values.

Analyst Coverage History

Disclaimer & Disclosure: We do own a long position in CRWD. This information is for research purposes only and is not investment advice. Please do your own research prior to any investment decisions. Past performance is not indicative or future results.

If you enjoyed this update, please subscribe so you can stay in the know with our upcoming notes!

If you are enjoying our equity coverage, please share us on social media or with friends and family who may be interested in the content.