Q2 Holdings - Fourth Quarter & Full Year 2020 Earnings Update

Q2 Holdings - Fourth Quarter & Full Year 2020 Earnings Update

Mid-Cap Financial Technology - COVID Headwinds Likely Behind Us; Accelerating Adoption of Digital Banking driving Durable Growth

Housekeeping note: We have not yet published our deep dive on QTWO. Since the company reported earnings this morning, we found an earnings update more timely and will be posting our deep dive in the coming weeks. Stay tuned! In the meantime, feel free to reach out to us with any questions or comments on the company.

Disclosure: We do own a long position in QTWO. Please read the remaining disclosures at the bottom of this post.

Q2 Holdings (QTWO) announced fourth quarter and full year 2020 earnings this morning. We have updated our estimates below to reflect the results and have included our thoughts on the quarter as well as notes from the company conference call.

Company Description

Q2 Holdings supplies cloud-based digital banking solutions to small and mid-sized banks. Their solutions enable customers to deliver robust suites of digital banking, lending, leasing and banking as a service (BaaS) that make it possible for end users to transact and engage anytime, anywhere and on any device. The company was founded in 2005 and became Q2 Holdings in 2013. They are currently headquartered in Austin, Texas.

Business Overview

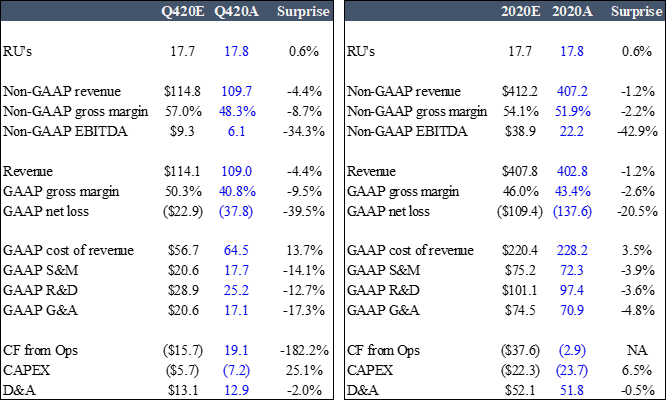

Despite a challenging economic backdrop emanating from COVID-19, the company reported a strong year, recording revenue of $407.2M, up 28% YoY. Q2 is exiting the year with 17.8M registered users (RU), setting a record for net adds in a year, and posting a YoY growth rate of ~22%.

Throughout the year, Q2 has seen continued expansion activity across their customer base, with new customer onboardings at record pace and a surge in digital banking activity prompted by the stimulus payments issued in the year.

On the sales front, Q2 had an impressive quarter with several notable deals closing. In the quarter, the team closed one enterprise and two Tier 1 deals. The enterprise win was with the US subsidiary of a top 10 global bank which selected Q2 for their loan data and enterprise coaching solutions. The first Tier 1 deal was also on the digital lending side, which is continuing to gain traction following the acquisition of PrecisionLender in the fourth quarter of 2019. The second Tier 1 deal was with an $8B bank who made the decision to replace their legacy commercial banking solutions with Q2’s corporate banking suite. The bank chose Q2 for their strong execution on their product roadmap and their ability to manage all customers from a single platform. Further, the same customer expanded their existing contract with Q2, speaking to the mission-critical nature of digital banking solutions coming out of the pandemic.

Throughout the year, the sales team signed 3 new enterprise customers, 13 Tier 1 customers and numerous new adds across Tier 2 and 3 customers. We this organic growth and cross-selling activity as bullish as it speaks to the accelerated adoption of digital banking and the broad platform capabilities that Q2 offers.

CEO Matt Flake reiterated the strength in cross-sale activity, mentioning strong demand for products like CardSwap, Centrix (risk management), and digital acquisition/onboarding solutions. The continued demand from customers signals to management (and us) that the pandemic has accelerated the adoption of digital banking features that provide for a more comprehensive and seamless user experience.

With regards to user growth and operational efficiencies, the company had two of their largest customer go-lives in the quarter, both within a two-week span with minimal hiccups. The delivery and hosting teams have been able to successfully navigate the pandemic environment and continue to deliver strong results for customers joining the Q2 platform. Further, because of the pandemic, Q2 customers issued hundreds of billions of dollars in stimulus payments, of which had to be facilitated by Q2 through PPP loan origination and forgiveness solutions. Within a few weeks, the technology and infrastructure teams were able to build out a solution that allowed the company to play a meaningful role in the distribution of stimulus payment across the country.

The role regional and community financial institutions (RCFI) play in our communities have been emphasized during the pandemic. The pandemic served as a reminder that without a network of thousands of RCFI’s, there’s no way that the stimulus payments and small business loans could have been efficiently delivered throughout the nation. With that in mind, the pandemic has acted as a catalyst for RCFI management teams to reconsider their long-term spending plans. The pandemic has shown us that digital banking is much less so a “nice to have” and is now mission critical infrastructure (“need to have”). With Q2, financial institutions can partner with a company who oversees ~$3.7T in commercial loan pricing data and more than 4B log-ins to digital banking platforms, offering a unique value-add.

Financial Highlights

Q2 reported results that exceeded the high-end of revenue guidance and near the midpoint of adjusted EBITDA guidance. Before jumping in to the results, we wanted to detail some accounting adjustments and impairment charges recognized in the quarter.

Accounting Adjustments & Contract Impairments

In the quarter, the company did alter their accounting for professional services. As the cloud lending business has matured and evolved, the company is aligning their accounting to recognize revenue over time as services are performed rather than as services are completed. At the same time, they are aligning their costs associated with those professional services to be recognized as they are incurred. The change in professional services accounting accelerated the recognition of revenue in the fourth quarter by ~$3.3M, accelerated costs by ~$4.2M. This change also reduced the associated deferred revenue and deferred implementation cost balances on the balance sheet.

The company also recorded a contract asset impairment related to the restructuring of a contract with one of Q2’s fintech customers, resulting in a ~$2.8M negative impact to revenue and gross margin. In discussing the impairment, management noted that Q2’s early exposure to fintech companies was primarily in early-stage companies with less-than-ideal financials. As Q2 has matured as a business, they have moved up the quality spectrum to avoid these situations and work with larger, better capitalized fintech companies. This impairment was the case of an early-stage fintech where they had to renegotiate some of the terms of the contract given financial instability with the customer. Management reiterated that this is not characteristic of the broader fintech customer base and that they are confident in their existing customer base in terms of financial soundness.

All in all, these adjustments resulted in a net increase in fourth quarter revenue to the tune of ~$467k. On the gross margin side, these adjustments were a ~$3.8M headwind, or approximately 370bps in Q4, 90bps in 2020.

4Q & FY 2020 Financial Results

For the fourth quarter of the year, Q2 recorded $109.7M of revenue, representing an increase of ~24% YoY. For the full year, the company reported revenue of $407.2M, +28% YoY. The growth in the year was driven by an increase in their subscription and service revenues associated with the deployment of new customers and incremental users on the platform as well as the continued success of PrecisionLender (which was acquired in 4Q19). Q2 ended the year with 17.8M RU, an increase of 22% YoY. The company added 36 new customers in the year, increasing the installed customers (IC) base (financial institutions) from 414 to 450. The growth in IC was attributable to increased customer go-lives and reduced M&A activity within their existing customer base. The potential resurgence in M&A activity could pose a headwind to incremental growth in IC’s over the next 12-18mo.

Q2 saw a slight tick up in churn in the year, increasing from 5.1% in 2019 to 5.9% in 2020. Management had been clear about their expectations for churn to increase a bit given increased customer mix with fintech’s playing a larger role than historically. Digital banking churn in the year remained sub-5% despite the impacts from the Q2 CARES initiative which provided short-term financial relief to their customers in exchange for extensions of their existing contracts. Throughout 2021, management expects churn to remain in line with 2020 levels despite the expiration of PPP contracts entered in 2020. Adding an additional complexity to churn, M&A activity in the smid cap bank market may increase which could impact churn rates. Historically, Q2 has been a net beneficiary from M&A, adding more customers than they lost during transactions.

Net revenue retention in the year increased from 120% in 2019 to 122% in 2020. Excluding the impacts of PrecisionLender, net revenue retention would have been 116%. Going forward, management estimates retention to remain ~115-120% range which has been relatively sticky historically.

Gross margin was 48.3% in the quarter, down from 56.8% in 4Q19. For the full year, gross margin was 51.9%, down from 54% in 2019. The accounting adjustments and contract impairments detailed earlier negatively impacted gross margins. Without the adjustments, 4Q and 2020 margins would have been 52% and 52.8%, respectively. The remaining decrease in gross margin was attributable to investments associated with increasing levels of engagement across various solutions and adding implementation and delivery resources to service the increased user growth.

Operating expenses for the quarter were $50.1M, +17% YoY and was driven by hiring of additional members of the R&D team. The company ended the year with 1,749 employees, up from 1,574 in 2019. The increases in R&D expenses were partially offset by decreases in S&M spending, which was impacted by lessened travel and conference activity due to the pandemic.

Adjusted EBITDA was $6.1M, down from $10.6M in 4Q19. For the full year, adj. EBITDA was $22.2M, up from $19.6M in 2019. Again, the accounting adjustments and impairments impacted the EBITDA numbers, reducing fourth quarter and full year adj. EBTIDA from $9.9M to $6.1M and $26M to $22.2M, respectively.

1Q21 & FY 2021 Guidance

Non-GAAP Revenue $114.6M-$116.1M, FY $488-$491M

Adjusted EBITDA $8.5M-$9.1M, FY $34.5-$36.5M

The team is expecting an increase in costs on the S&M side (coming off relatively low base due to COVID restrictions on travel). Guidance does assume a resurgence in these costs in the back half of the year as well as increased hiring activity throughout the year.

Additional Comments

Incremental Customer Demand

Conversations with customers remain constructive on the digital adoption of the regional and community banking industry. CEO Matt Flake thinks the focus on digital initiatives will come back and will see incremental sales momentum.

Tier 2 and Tier 3 deals were steady in 2020 – they didn’t quite hit Q2’s pre-COVID plan but Tier 2-3 deal scene was much steadier than Tier 1, which completely dried up throughout the year. The pipeline is seeing Tier 1 customers come back on line with real engagement and real budgeting (not just top of the funnel conversations). We don’t expect anything material in 1H21, but could see a return to 2018-2019 growth levels on the new customer go-lives in the back half of 2021 into 2022.

While the Tier 1 activity picking up is a great sign for the long-term growth for the company, Tier 1 deals will typically follow a 12-18mo lag time to get to profitability. The team is excited about the pipeline but its key to understand that deals done in 2021 wont fully materialize into revenue until 2022. Management has factored the impacts of the implementation timeline into their 2021 guide and are confident in the 20-21% growth range implied by guidance.

On the question of a wholesale re-platforming amongst RCFI’s, management mentioned that Tier 1 conversations are more about strategic planning. The implementation of Q2 solutions is much less about speeding up the implementation process and much more about the operational readiness of RCFI’s and their ability to adapt and innovate. Many banks will try to time new go-lives to coincide with ending contracts and time frames are tight so it’s very rare to have a wholesale re-platforming. In a typical relationship, a customer will launch one solution, say for example their retail banking solution, and have that running for a few months. As the relationship gets built out and customers (hopefully) have a good experience, they often cross pollinate. This is one of Q2’s biggest strengths: the broad capabilities offered in their platform offers the opportunity for robust cross-selling, which we have seen play out over the last 12 months. As they work with customers to build out a product roadmap, they can strategically offer solutions to tailor to their customers needs all on one unified platform.

ARPU

Slight decline in ARPU in the year, driven by the beneficial pricing of the PPP loan programs. The team is confident about the long-term impacts of servicing those clients throughout COVID. They are expecting a tick up in ARPU in 2021 driven by increased penetration of existing clients and incremental value added with new products. On a go-forward basis, the primary driver of ARPU will be from cross-sale activity with existing clients and further penetrating into their institutions.

In our view, the year went largely as we expected (given the economic backdrop). We are curious about the accounting adjustments and the plan for gross margins on a go-forward basis and will dig deeper into this when the 10-K gets released. With 2020 behind us, we look forward to the robust customer pipeline coming through in the back half of 2021 into 2022. We believe the adoption of digital banking solutions will remain a key driver of the business. With incremental conversations with RCFI management teams being very constructive, we believe the activity coming through the pipeline will allow a return to growth acceleration for the business after a slowdown in 2020 (due to customer go-lives being pushed back).

All in all, we are pleased with the resilience of the company. We think that the pandemic has solidified Q2 solutions as a “need to have” rather than a “nice to have”. With management mentioning strength in the pipeline, notably in their Tier 1 banking customers, we are confident in the company’s ability to continue to close new deals and expand with existing companies through their cross-selling efforts. We believe that existing cross selling efforts and organic ARPU growth will drive operating margin expansion over the medium term to in-line with competitors ~15-20%.

Valuation & Intrinsic Value Update

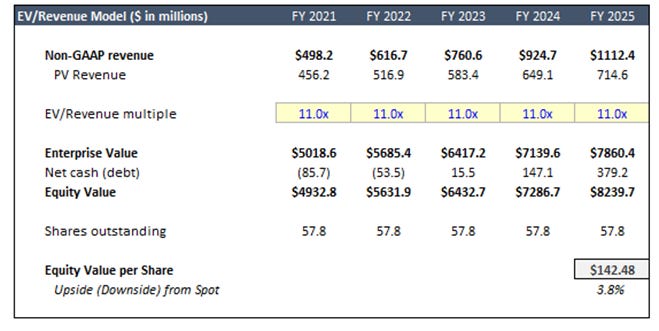

We value QTWO with a 5Y EV/Revenue multiple. We apply a WACC of 9.3% to their forecasted revenues through 2025 and apply a multiple of 11x, a slight premium to peers we think is justified given superior growth and a broader product platform. This assumption gets us to a $142 estimate of intrinsic value, slightly ahead of the stock price at the time of writing. The stock has had a great beginning to 2021 and has run quite a bit; we believe the stock is currently around fair value. The company remains a key beneficiary of digital banking trends and broader financial technology adoption and we are confident in their ability to maintain a durable ~20-25% revenue growth rate over the medium term.

Model Summary

Multiple Model

Risks to the estimate include:

COVID-19 remains a key risk to the thesis. QTWO has seen customer go-live delays and PPP/SBA services pose transitory headwinds to the business. Our base case assumes a normalization of economic and societal activity. In the case there is a resurgence in COVID-19, we will have to re-evaluate our top line assumptions for customer go-lives.

Operational execution – With lag times for most customer go-lives being in the range of 12-18mo, operational execution and planning is critical to the success of the business. In the case there is a deterioration of business strategy or operational execution, we would re-evaluate the growth prospects for the company.

Broader adoption of digital banking – While we believe it is a near-certainty that digital banking trends are here to stay and have been accelerated by COVID-19, in the case RCFI’s do not engage with the theme, the thesis for Q2 will be materially impacted. We believe the increased pipeline activity and constructive conversations management mentioned on the call this morning help give us confidence that this will not be the case.

Analyst Coverage History

Disclaimer & Disclosure: We do own a long position in QTWO. This information is for research purposes only and is not investment advice. Please do your own research prior to any investment decisions. Past performance is not indicative or future results.

If you enjoyed this update, please subscribe so you can stay in the know with our upcoming notes!